With hundreds of credit cards now available in the market, it can get really confusing especially when you consider the fact that not all of them are created equal. However, these days many Malaysians optimise their credit cards spending with cash back credit cards.

Essentially, a cash back credit card is a credit card that rewards the cardholder a rebate based on their spending. This can be then further broken down into the cash back tier, monthly cap and cash back categories.

Cash back tier means how much you have to spend to earn that amount of cash back. For example, if you spend RM300 you get 4% cash back and have to spend RM2,500 and above for 8% cash back.

Next up is the monthly cap which is the amount that the rebate is capped at every month (ranging from RM10 – RM100 or more), and the cash back category is the type of retail transaction or spending you need to perform to qualify for the cash back rebate.

However, if you are looking for a cash back credit card that suits your spending habits, we’ve shortlisted three of the best ones for you to choose below.

Hong Leong Wise Gold Card

Looking for a cash back credit card that offers you a variety of choices on the cash back categories?

The Hong Leong Wise Gold lets you enjoy 10% cash back on spending for two of your chosen

categories (there are ten available) when you make a minimum of any 10 retail transactions

(minimum RM50 per transaction) in a month.

Do take note that to change categories at any time,

you will have to pay maintenance fee of RM10.60.

Recommended for:

Malaysians who use their credit card for a variety of transactions and want more control on their cash back based on their spending habits.

Qualifying Criteria:

- Minimum age of 21 years old and a minimum income of RM2,000 per month (RM24,000 per annum)

- Annual fees: RM169.90 for Principal cardholders and RM84.80 for supplementary card holders

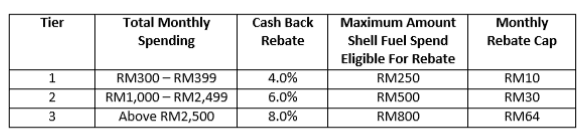

Shell-Citi Gold Credit Card

Always on the road or just want more money back from all your petrol expenditure? The Shell-Citi Gold credit card lets you enjoy a cash back rebate of up to 8% when you fill up on petrol at any Shell station nationwide.

Recommended for:

This cash back credit card is ideal for Malaysians who spend more on petrol every month and prefer to visit Shell petrol stations to earn cash back rebates.

Qualifying Criteria:

- Minimum age of 21 years old and a minimum income of RM2, 000 per month (RM24,000 per annum)

- No annual fees for the first year by using the card three times within 60 days of card approval.

- For subsequent years, RM206.70 per annum for principal; RM106.00 for supplementary cardholders.

OCBC 365 MasterCard

The OCBC 365 MasterCard is a great choice if you are a first time credit card owner looking to earn cash back on all of your spending.

You will receive 1% cash back on the first RM1,000 you spend and 0.5% for all subsequent spending – making it a hassle-free and easy to manage cash back credit card.

Recommended for:

Malaysians who are looking for their first credit card and wish to enjoy cash back rebates for all of their spending.

Qualifying Criteria:

- Minimum age of 21 years and a minimum income of RM2,000 per month. (RM24,000 per annum)

- No annual fees for the first year, only for first time OCBC credit card customers or customers who last held an OCBC credit card more than 12 months ago.

- RM106.00 per year for principal and RM53.00 per annum for supplementary cardholders.

For more information on how to compare cash back credit cards, check out this handy guide

here by CompareHero.my.

Note: This is a guest post by CompareHero.my, a Malaysia’s financial comparison portal which helps consumer in finding the right financial products at the right price.