Kenanga Digital Investing (KDI) has been around for a few months since early 2022, and I have just joint on the bandwagon last week.

KDI is a robo-advisory investment platform under Kenanga Investment Bank. It can be accessed either using web browser to its website, or via its mobile app available for Android and iOS.

FYI, this is the same Kenanga Investment Bank which has another popular investment platform called Rakuten Trade for online stock investment.

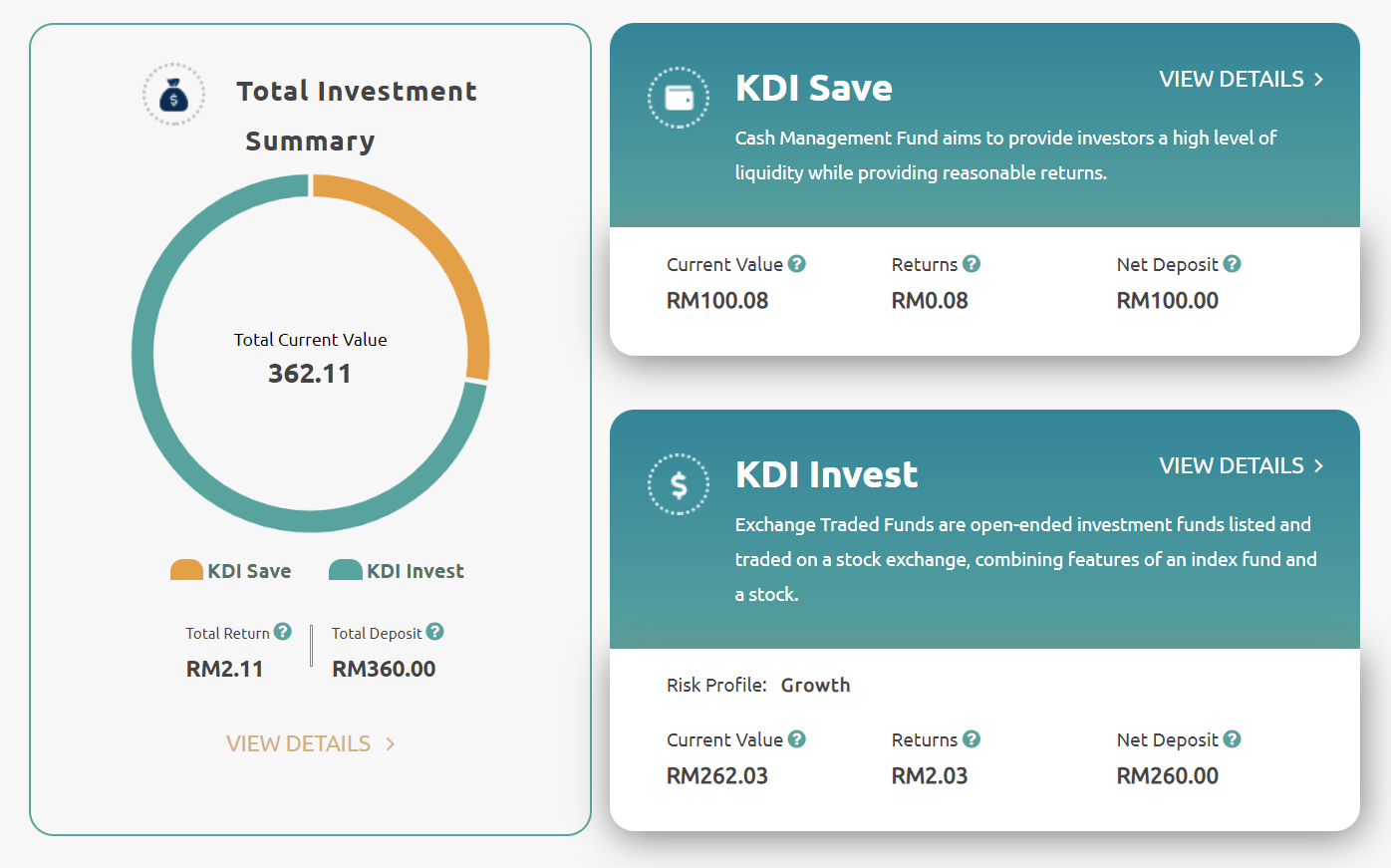

I just put in the minimum starting fund requirement of RM100 in KDI Save and RM250 in KDI Invest respectively for a trial to test its performance. I've used my friend's referral code during registration and got RM10 as a result. Therefore, my invested amount in KDI Invest has become RM250 + RM10 = RM260.

After invested for about a week, this is my portfolio performance so far.

My KDI Save has gained RM0.08 (0.08%) from RM100, equivalent to 2.92% p.a over a period of 10 days.

My KDI Invest has gained RM2.03 (0.78%) from RM260, equivalent to 28.49% p.a. over a period of 8 days.

I would say, this investment result is pretty impressive. Hope that KDI can keep up this kind of performance for a long period of time.

Currently, KDI only has 2 investment products: KDI Save and KDI Invest.

KDI Save is similar to

Opus Money Plus Fund (MPF),

Touch n Go (TNG) GO+, StashAway Simple, and other money market fund (MMF). It is quite impossible to incur losses, and its return is expected to be just slightly higher than the bank's fixed deposit rate. This is a kind of investment of low risk low return.

KDI Save's return is daily calculated and daily credited into your account. Currently, for an investment amount of RM100, you can get RM0.01 per day. KDI does not incur any management fee, pretty similar to fixed deposit savings with bank.

KDI Invest is an A.I. operated ETF investment fund. It invests into ETF funds listed in the US market, which coverage is around the world.

The investment profit or loss of KDI Invest is daily updated in its returns value. Being an ETF fund, its fluctuation is pretty small.

You can decide your KDI Invest portfolio risk profile to be set as either Very Conservative, Conservative, Balanced, Growth or Aggressive Growth. That will determine the level of fluctuation of your daily profit or loss.

Invested amount of RM3,000 or less in KDI Invest is free from fund management fee. More than that, there will be a management fee of 0.3% to 0.7% per annum. On top of that, there is also an ETF transaction fee of 0.2% to 0.4%. per annum. This amount of fund charges is considered very minimal, compared with the charges of majority of the mutual funds in the market.

If you want to get an additional RM10 in your KDI Invest account, you can sign up using this

referral code:

114053

After signing up, before you can gain access to KDI and start investing, you need to wait for 1 or 2 days for the processing of your KYC verification. You will receive an email from KDI once your account application is approved.

Please remember that, in order to get your RM10 for using my

referral code:

114053, you are required to transfer a minimum of RM250 from your bank account to KDI Invest within 30 days upon account creation. If your KDI Invest account is not activated with an initial investment after the expiry date, you will miss your opportunity of getting that RM10.